In 1952, the California State Legislature authorized TIF (Tax Increment Financing) districts to improve economic conditions in “blighted” areas. Currently, over 10,000 TIF districts are dispersed across 49 states. Yet, TIFs usually siphon funds from public services. Statewide and local case studies highlight this deficiency. Luckily, a bevy of underutilized reforms can tackle the issues of housing affordability and economic development that TIFs theoretically promise, yet practically fail to solve.

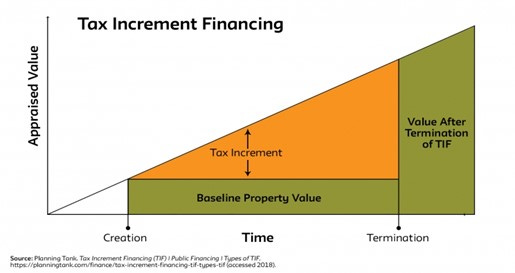

A TIF district is established when the property values in a designated area are frozen at a base rate. Tax revenues are collected on this frozen valuation, typically for 20-30 years. Revenues generated beyond the base value are earmarked in a separate fund distributed to private investors and developers through economic development loans or subsidies.

This financing typically takes one of three forms:

1. “Pay-as-you-go,” where the incremental revenues cover project expenses over time.

2. The developer issues debt intending to use the incremental revenue as reimbursement.

3. The local government issues debt via a general obligation or revenue bond with the goal of incremental revenue covering future principal and interest payments.

Transparency Issues

It is challenging to attribute developers’ decisions to the lure of TIFs. Additionally, local governments are hobbled in guaranteeing that a TIF’s promises can come to fruition.

Most states require TIF projects to contain a “but for” clause. This provision supposedly verifies that the developer would have declined to pursue the project without the TIF; however, this is a misnomer. States do not grant local governments the authority to review the internal documents of firms. Board minutes or emails relevant to the project might provide valuable information regarding the “but for” claim.

Yet, if this data remains proprietary, there is no mechanism for corroborating the claim. Developers do not have to disclose their decision-making process yet get to claim a subsidy on the assumption that this information asymmetry does not exist.

Accountability Issues

TIFs are less transparent and accountable than other controversial subsidies or incentives. For example, a corporate income tax credit enables companies to deduct a portion or all of their business expenses from their tax bill. While this is not a panacea for local economic development woes, prudent local governments can enact, at least, some minimum guardrails.

These agreements can include stipulations that their annual renewal is contingent on the company creating X number of jobs at Y prevailing wages. Moreover, clawback provisions can help local governments recoup taxpayer dollars from companies that fail to uphold their end of the bargain regarding promised public benefits like job creation.

TIFs do not avail local governments of such recourse. The most common types rely on debt service. Therefore, bondholders are entitled to the principal and interest payments once a bond is issued. Revisions based on TIF district performance and impact are impermissible upon the bond issuance.

The only option would be for the local government to refuse to make debt service payments – which would be considered a default on the loan and lead to significantly higher future borrowing costs.

Chicago

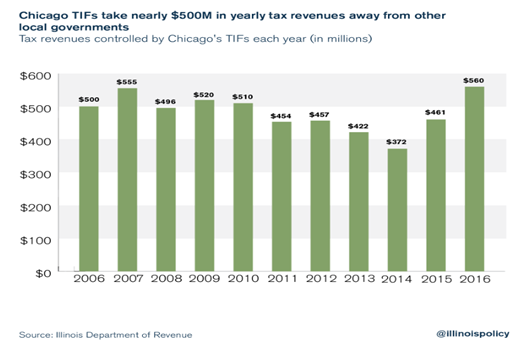

At 143, Chicago has the most TIF districts out of all U.S. cities (more than the following nine most populous cities combined). The TIF revenues are collected in a separate fund and then rewarded by the mayor to private developers typically looking to build in wealthy areas – like Navy Pier – the city’s most popular tourist destination. For example, from 2006-2016, $2.5 billion of property tax revenues were redirected from Chicago Public Schools (CPS) to TIF districts.

CPS receives 50% of Chicago’s property tax revenues, yet TIFs comprise 10% of the city’s total property value. These revenues might have helped prevent at least some of the 50 CPS school closures in 2013 alone. Attempts to shore up this revenue gap lead to a dynamic where property tax rates increase, despite home values decreasing.

In 2019, Mayor Lori Lightfoot championed a host of TIF reforms. These tweaks included a more stringent “but-for” test linking the TIF to surrounding development, published monthly data showing TIF activity, and an annual report explaining the TIF process to residents.

Yet in 2022, Chicago halted the expiration of 11 TIF districts with combined revenues and collective fund balances of $158 million and $509 million, respectively. Their expiration would yield tax savings for homeowners and more significant revenue for public schools and the city’s general fund, even at a lower tax rate.

California

California exemplifies how TIFs amplify the fiscal issues stemming from state property tax caps. In 1972, the legislature pledged a $2 billion reimbursement for schools that lost funding to TIFs. However, this subsidy proved insufficient once the property tax cap imposed by Proposition 13 in 1978 magnified the revenue shortfall. As property tax revenues declined, cities created additional TIF districts to attract substantial business sales tax revenue. This resulted in more funds being redirected from public schools to TIFs. As the state earmarked additional funds to shore up this revenue shortfall, a vicious cycle emerged where the fiscal health of TIFs and public schools was almost directly tied to that of the state.

In 2012, as the state faced increased fiscal duress, Governor Jerry Brown temporarily dissolved the redevelopment agencies that administered TIFs, effectively terminating them. A study discovered that only four out of 38 TIFs in the counties of Los Angeles, San Bernardino, and San Mateo were self-financing influenced his decision.

Austin

Even in fiscally healthy governments, TIFs typically function as a slush fund for politicians, developers, and investors rather than as a vehicle for economic redevelopment. For example, two of the City of Austin’s four TIF districts encompass affluent areas. The average rent in Austin for a one-bedroom apartment is $1,518/month. Two of its TIF districts, Seaholm and Mueller, rank sixth and first among least affordable neighborhoods, with average monthly rents of $2,629 and $3,963, respectively.

The city is losing significant amounts of money by maintaining the TIF designation for these neighborhoods. Seaholm was established as a TIF district in 2008, with a base taxable value of $6.6 million. In 2019, its total property valuation ballooned to $309 million; however, only the $6.6 million is taxable until the TIF status expires in 2041. Mueller was designated a TIF district in 2004, with a base taxable value of $0 – since the City of Austin owned the land. In 2019, the total property valuation of the neighborhood skyrocketed to $1.4 billion. Yet, none of this amount will be taxable until the TIF designation expires in 2045.

Vermont

In 1985, Vermont introduced TIFs with a conscious regard for ensuring equitable outcomes. Whereas most states authorize TIFs for private development without geographic restrictions, Vermont confines them to public infrastructure projects located within a city’s downtown. Additionally, the TIF must achieve at least one public benefit, including affordable housing, brownfield clean-up, or an expansion/improvement of transportation options. Finally, unlike most states, Vermont also requires developers to sign guarantees where they pledge to hit specific construction benchmarks within a predetermined amount of time. Construction is not permitted until this agreement is brokered.

Vermont presents a compelling case study highlighting the extent to which fundamental issues of inequity plague TIFs. The robust measures enacted to temper their disparate outcomes fall short.

The Vermont Legislative Joint Fiscal Office (a non-partisan agency that provides fiscal analysis to state legislative committees) analyzed the impact of TIFs on the state’s Education Fund. From 2017-2023, the TIF program is estimated to divert $3 million - $6 million from the Education Fund. In the upcoming years (2023-2028), these projections increase to $7 million - $8 million. These trends result in a forecasted cumulative loss of $68 million for the Education Fund.

Methodologically, the Joint Fiscal Office (JFO) compared current and projected revenues based on collected property taxes if no TIF existed relative to base property tax revenues allocated to the Education Fund under the current TIF regimes. Proponents might argue that once the TIF designation expires, this will hypothetically lead to an influx of previously untapped revenue. The idea is that forgoing immediate revenue for a few decades will yield greater long-term returns for schools and local governments. Yet, it is uncertain when, or even if, this geyser of funds will erupt and shower communities with a bevy of newfound opportunity and prosperity. For example, the JFO estimates that it will, on average, take 50 years from the inception of a TIF district for its cumulative revenues to the Education Fund to break even with those of the same area absent a TIF.

The JFO’s analysis modifies the flawed “but for” premise of TIFs, which assumes no baseline property tax revenue would have materialized sans the TIF. It incorporates a county’s average property tax revenue growth 20 years before creating a TIF district. This prevents TIF revenue projections from overemphasizing economic slumps, providing a more holistic view of these trends.

While TIFs may have been introduced with good intentions, their outcomes perpetuate and exacerbate economic and social inequities within cities. TIFs are one of the most popular economic development tools used nationwide. If TIFs were terminated or reformed, the revenue stream could be used to adequately fund schools and essential city services. Nevertheless, Vermont demonstrates how even good faith attempts to reform TIFs fail to mollify the flimsy premise that grants them legitimacy.

TIF Alternatives

The ubiquity of TIFs should not lull us into accepting their inevitability. The United States is in the thick of a housing affordability crisis. For example, there is a shortage of 7 million affordable homes (“affordability” defined as housing expenses not exceeding 30 percent of monthly income). Thus, for every 100 low-income renters, only 37 affordable homes are available. A slew of proposals – like revitalizing government construction of public housing, zoning reform, a land value tax, and Community Land Trusts (CLTs) can hit the nexus of affordability and economic growth.

A. Public Housing

In 1998, the Faircloth Amendment revised the Housing Act of 1937 to cap the public housing supply. It froze the number of units per local public housing authority to 1999 levels. However, a dearth of federal funding is an even more pernicious issue affecting the public housing supply. For example, Faircloth’s limits allocate 35,453 units to the Chicago Housing Authority. Yet, it only operates and maintains approximately 21,000 units. The Philadelphia Housing Authority is allocated 20,133 units, but only around 14,000 are operational.

Since the 1980s, the federal government has perpetually underfunded public housing. This trend culminated in a $26 billion backlog of unaddressed maintenance and repair issues in 2010. Federally funded public housing has a checkered reputation which is primarily a function of the racially segregated and insufficiently funded implementation of public housing. As such, it is not a reason to throw the baby out with the bathwater. Cities like St. Louis, Chicago, and Washington D.C. approved highways that separated these communities from the urban core. Revitalization of public housing does not require repeating the past’s mistakes. Unlike TIFs, federally funded and locally administered public housing is not dependent on developer and bondholder middlemen who profit at the expense of local communities under the auspices of ameliorating “blight.”

B. Zoning Reform

Local land development codes make housing construction cumbersome. For example, approximately three-quarters of all city land nationwide is reserved exclusively for constructing single-family homes. Redressing the paucity of affordable housing is practically insurmountable whenever the construction of apartments, duplexes, townhomes, or accessory dwelling units (ADUs) is illegal on most land in most cities. Minimum lot sizes/setbacks, building height caps, and minimum parking requirements (hence why nationally, there are four parking spaces per car) further hinder multi-family housing construction.

Minneapolis provides a compelling case study for emerging zoning reforms. In 2018, the city council prohibited minimum parking requirements and authorized multi-unit housing construction on tracts previously zoned for detached, single-family homes. This combination of reforms bolstered the number of annual building permits, including approximately 2,600 units from 2013 through 2017, to around 6,500 units from 2018 through 2022.

Unlike TIFs, tweaks to the land and development code do not require municipalities to forgo revenue. Instead, they widen the tax base and lower housing costs by increasing the housing supply. Additionally, they encourage local government officials to tackle systemic problems rather than focusing on piecemeal solutions. Approving a TIF district might be politically expedient for an upcoming re-election, and proposing zoning reforms is likely to yield an aggressive response from neighborhood associations. Still, the Sisyphean rock of the housing crisis will not abate unless addressed systemically.

C. Land Value Tax

Tax breaks are not inherently a state and local government gamut to stimulate development in downtrodden areas. Instead, tax restructuring in the form of a land value tax can achieve this outcome. Under this proposal, the land is taxed, but the property on the grounds is not.

Under a conventional property tax system, residential or commercial building improvements typically trigger a concomitant tax increase. Thus, developers lack the incentive to build or improve. Land tends to appreciate for “sitting there,” yielding an unearned investment since it does not produce any accompanying economic output. Notably, the Federal Housing Finance Agency discovered that from 2012-2018 land prices rose at a significantly higher rate than home prices in the nation’s largest metropolitan areas.

Transitioning to a land value tax might also offer an alternative to local government overreliance on broadly regressive property tax revenues. Nationwide, the bottom decile of neighborhoods pays a higher effective property tax rate than the wealthiest 10 percent. This divergence is primarily caused by information asymmetry between assessors and homeowners. Assessors are legally confined to observing a home’s exterior. Therefore, they are unaware of renovations that occur in greater frequency and scale within wealthier neighborhoods.

While a pure land value tax cannot be found in any American municipality, several administer a “split rate” system. For example, in 1982 Harrisburg, Pennsylvania, enacted a split rate system with a 4:1 ratio, where land is taxed at a rate four times higher than buildings. At this time, Harrisburg was considered the second most distressed American city per federal distress criteria. From 1982-2001, vacant structures dipped from around 4,200 to under 500. Moreover, the number of businesses on the city’s tax roll ballooned from 1,908 to 8,864.

Unlike TIFs, a split rate system provides a unique opportunity for local governments to lower taxes on the economically vulnerable while expanding the overall tax base and not hobbling essential public services.

D. Community Land Trusts

Under the CLT model, a board consisting of CLT residents, public officials, non-profit leaders, and non-resident general members uses a combination of public and private funds to acquire land. The CLT then leases the land for 99 years (a ground lease with monthly charges usually below $100) to middle or low-income residents. This shared equity model enables residents to own the home (the CLT still owns the land underneath in perpetuity) and receives a portion of home sales proceeds, with the bulk of proceeds going to the CLT – typically split 25-75. Resale restrictions ensure the home remains affordable after being transferred to a new owner.

Unlike TIFs, CLTs tangibly cater to low-income individuals and families. Nationally, the majority of CLT residents are low-income (51 percent – 80 percent Area Median Income [AMI]), first-time homebuyers and 95 percent of CLT homes are affordable for those earning 80 percent AMI or less. While TIFs can spur displacement, CLTs provide stability for low-income households. CLT residents are around seven times less likely than all households to move during any given year. Furthermore, in 2010 the foreclosure rate of CLTs was around ten times lower than that of homes in the conventional market.

There are only 225 CLTs nationwide, compared to over 10,000 TIF districts. CLTs provide stability and wealth to low-income households, while including diverse community stakeholders in housing and development decisions.

While none of these four alternatives is a nostrum for economic development and affordability issues, they warrant further examination. None of them have achieved the scalability of TIFs, yet their current implementation demonstrates promising results. All levels of government must decide if developer interests will continue to supersede structural reforms.

I had no idea what a TIF was until today, thanks for the education!